Explore

In the fast-evolving world of sustainable finance, one instrument is quietly redefining how companies link business performance with climate accountability: the Sustainability-Linked Loan (SLL). Unlike traditional green loans, which fund specific environmental projects, SLLs tie a borrower’s interest rate to their sustainability performance targets (SPTs). If a company meets pre-agreed goals-such as reducing emissions or improving workforce diversity- it earns a lower interest rate. Miss the mark, and the rate climbs.

It’s a simple but powerful idea: sustainability as a lever of profitability.

The global SLL market has expanded rapidly in the last few years. According to BloombergNEF, cumulative sustainability-linked loan issuance surpassed USD 1 trillion in 2024, a 10-fold increase since 2019. Another report by BBVA Corporate & Investment Banking shows that sustainability-linked loans accounted for over 60 % of all sustainable-loan activity worldwide last year.

India, too, is catching up. Economic Times reports that Indian banks such as SBI, HDFC Bank and Axis Bank are actively exploring SLL frameworks with large industrial borrowers in sectors like chemicals, manufacturing, and renewables. With the government’s commitment to achieve net-zero emissions by 2070, SLLs could emerge as a key financial driver of corporate transition.

SLLs stand apart because they are use-of-proceeds agnostic-borrowers can apply funds to any purpose, provided they commit to measurable sustainability outcomes. This makes them attractive to companies in hard-to-abate sectors (cement, aviation, steel, etc.), where decarbonisation is a gradual journey.

The Loan Market Association’s Sustainability-Linked Loan Principles (SLLP) define four core components:

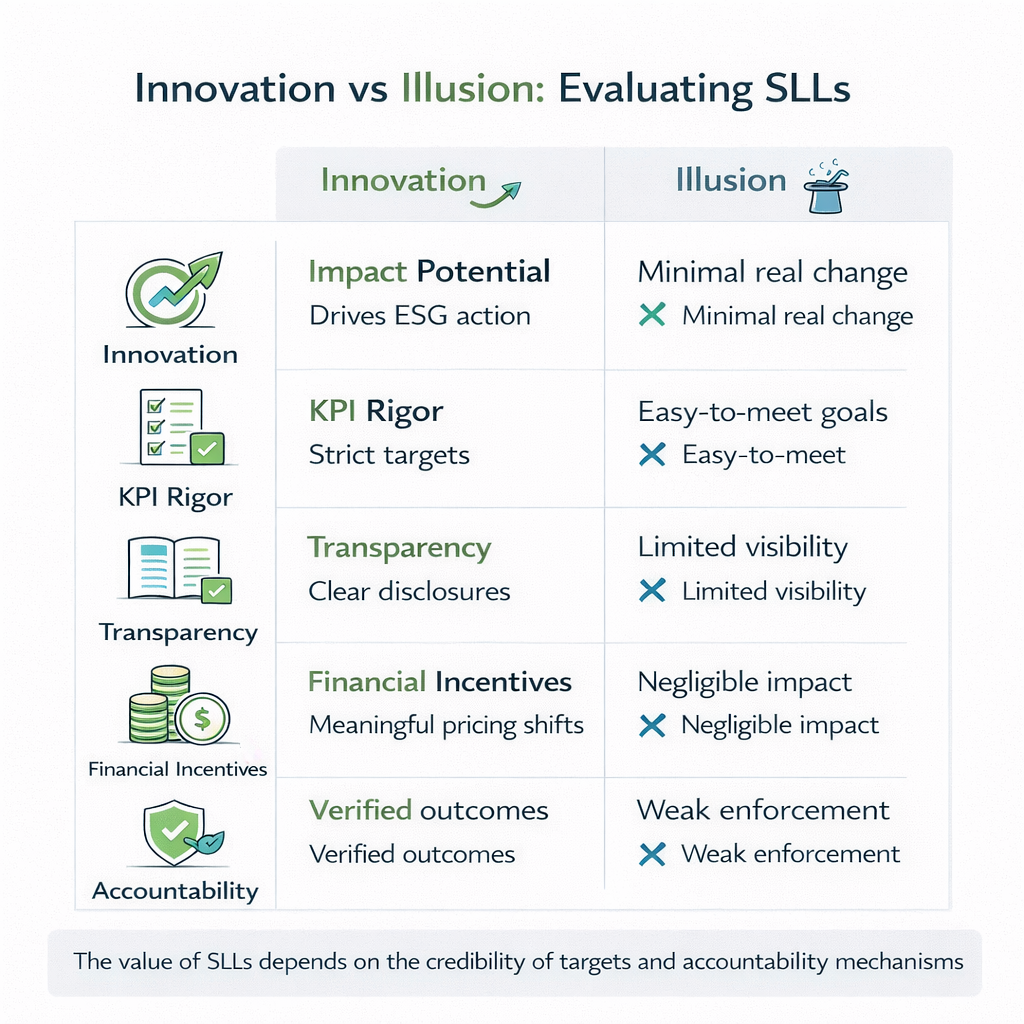

This framework embeds sustainability into the DNA of corporate finance, turning ESG performance into a tangible cost-of-capital factor.

The appeal of SLLs lies in their win-win narrative: businesses save on financing costs, and lenders can demonstrate ESG-aligned deployment. However, this innovation carries growing scrutiny.

Research by S&P Global warns that many SLLs risk greenwashing where KPIs are too lenient or poorly verified. Some firms set goals they were already on track to achieve, diluting the loan’s additionality. Others self-report progress without third-party audits, creating credibility gaps.

In India, the challenge is even sharper: inconsistent ESG data, varying disclosure quality, and a lack of standardised benchmarks can undermine the effectiveness of such instruments. Regulators like SEBI and the RBI are exploring frameworks to align SLLs with broader sustainable-finance guidelines, ensuring transparency and accountability.

A sustainability-linked loan is only as credible as its KPIs. The LMA recommends that KPIs should be relevant, measurable, and ambitious, but enforcement varies. For example, a company pledging to cut emissions intensity by 5 %, without reducing total emissions, might still qualify for interest benefits.

To ensure real-world impact, lenders and borrowers need sector-specific KPI playbooks. Heavy industries should focus on carbon intensity; consumer sectors on ethical sourcing or circularity. India’s upcoming green taxonomy could play a vital role in standardising such metrics and linking them to national climate priorities.

Innovation without oversight risks eroding trust. In 2025, regulators in the EU, UK, and ASEAN introduced new disclosure norms for sustainability-linked debt to prevent greenwashing and improve verification standards. India is likely to follow suit, strengthening its own ESG-finance ecosystem.

For corporates, the message is clear: transparency and third-party validation are non-negotiable. For lenders, it’s time to ask harder questions and resist the temptation to issue “ESG-branded” loans without credible substance.

Sustainability-linked loans are not just a financial instrument. They’re a reflection of how capital markets are evolving toward accountability. For professionals in finance, ESG, and corporate strategy, understanding how these instruments work and how to evaluate their credibility is becoming an essential leadership skill.

The IIM Kashipur – PG Executive Program in Net Zero Strategy & Sustainability Leadership, offered in collaboration with evACAD, empowers professionals to navigate this new financial landscape. The program covers critical areas such as sustainable finance, carbon markets, ESG integration, climate policy, and green innovation, enabling participants to evaluate and structure mechanisms like sustainability-linked loans with rigour.

Through live online sessions, expert faculty from IIM Kashipur & Industry, and immersive campus learning, participants gain both strategic and analytical mastery-preparing them to lead in a global economy that rewards sustainability performance as much as profitability.

Sustainability-linked loans are neither an illusion nor a silver bullet. They’re a bridge between today’s financial systems and tomorrow’s sustainable economy. Their impact will depend not just on the scale of issuance, but on the integrity of design and the leadership behind implementation.

As sustainable finance becomes mainstream, India has the opportunity to set global benchmarks. And for professionals ready to shape this future, programmes like IIM Kashipur’s provide the perfect foundation to lead with insight, credibility and purpose.

.webp)

.jpg)