Explore

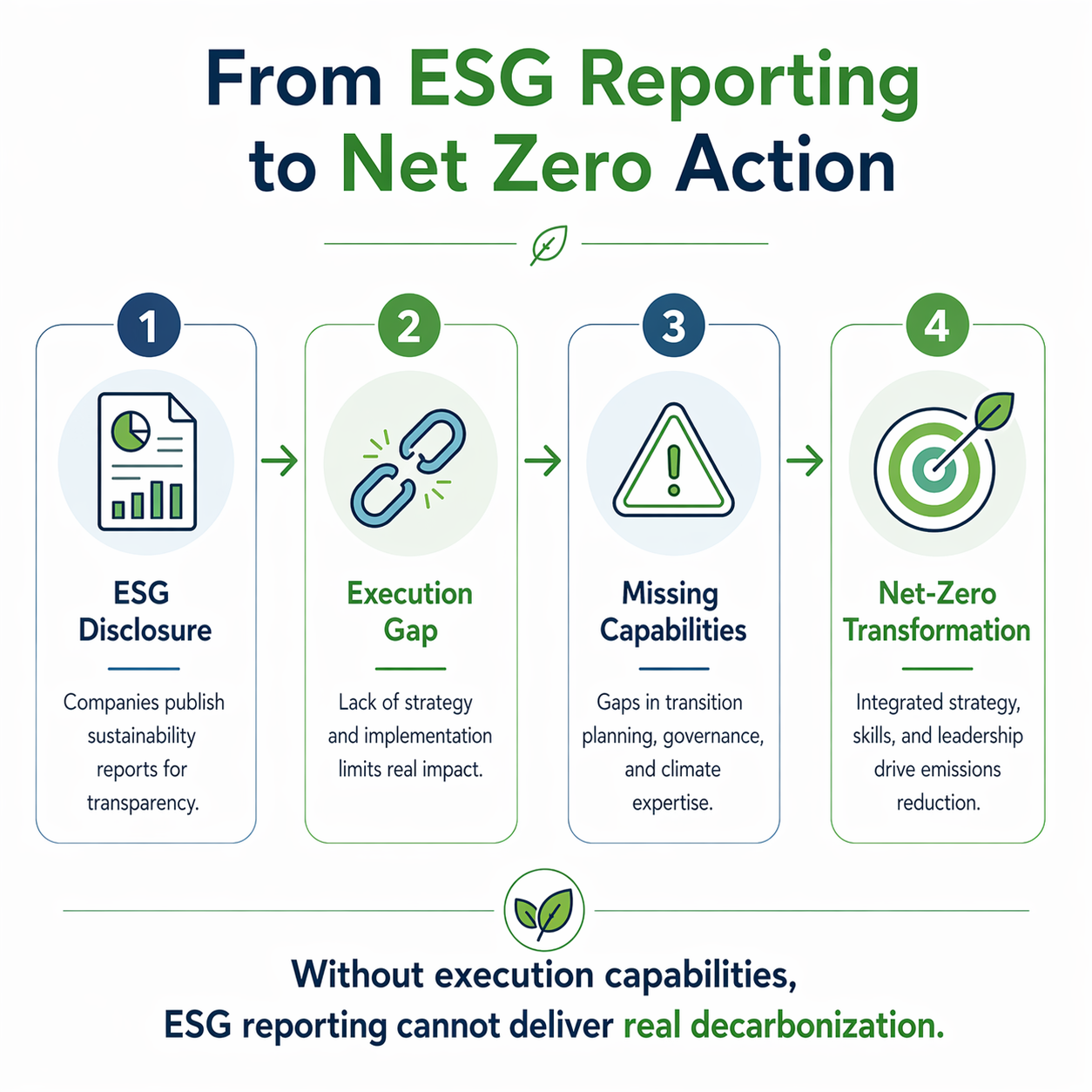

The board approves the net zero commitment. The sustainability team completes the carbon footprint calculation. Finance publishes the ISSB S2 disclosure. Progress appears complete, yet operational reality remains unchanged.

The operations director needs clarity on which capital expenditure proposals align with decarbonization pathways. Procurement continues selecting suppliers based on price and delivery performance while overlooking carbon intensity. The head of strategy struggles to translate a 1.5°C scenario into measurable business model implications.

Research by the Chartered Management Institute, covering organizations across the UK economy, found that 57 percent of managers working in companies with net zero plans reported insufficient clarity regarding their role in implementation (1). This capability gap directly constrains execution.

Organizations require leaders who can operationalize net-zero strategies across functions, develop transition plans that withstand board scrutiny, and integrate carbon considerations into commercial decision-making based on sustainability and climate change.

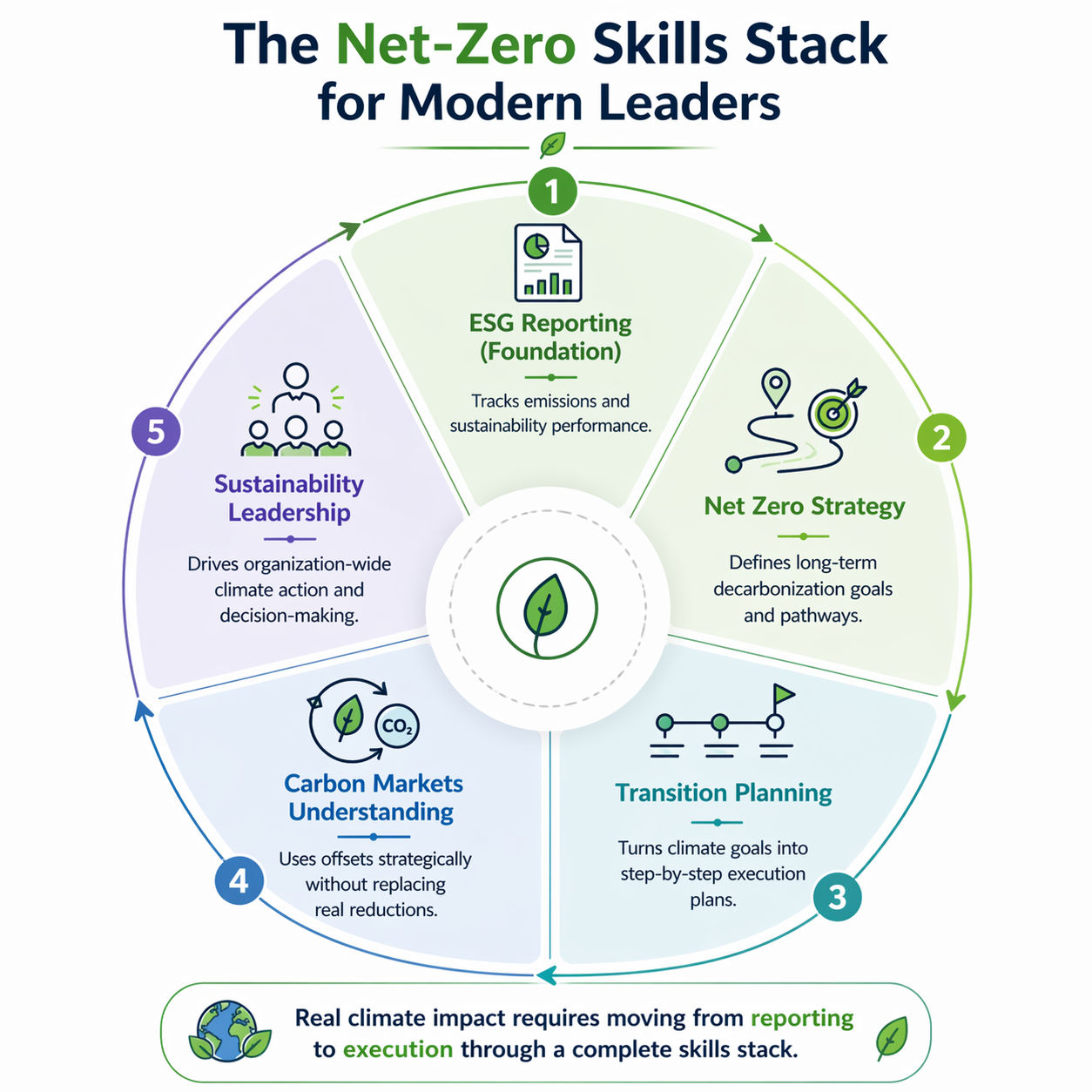

The net-zero skills stack consists of three essential skill sets that organizations need to implement their climate commitments through operational changes. The components of these systems include transition planning methods, carbon accounting systems, climate scenario assessment tools, and regulatory compliance systems, together with sustainability leadership capabilities for decarbonization.

Finance directors require knowledge about Scope 3 materiality assessments, which they need for their work. Supply chain leaders need to create supplier engagement programs that meet the requirements of the Science Based Targets initiative framework (5). Product development teams need to use life cycle assessments to establish their design standards.

The International Sustainability Standards Board ISSB S2 standard requires companies to disclose their climate change risks and their plans to transition to sustainable operations (6). The Task Force on Climate-related Financial Disclosures framework requires organizations to conduct scenario analysis, which shows their ability to endure different temperature scenarios (7).

These activities go beyond basic reporting requirements. The researchers require organizations to have three essential capabilities, which include strategic planning and capital allocation modeling, and operational redesign.

Sustainability teams can calculate emissions inventories. The establishment of internal carbon pricing systems fails because organizations do not include these systems in their financial decision-making processes. CFOs need to see direct business connections that show how decarbonization will improve their company's competitive position.

The operations teams need to receive instructions that will help them create new manufacturing systems that will eliminate their need for thermal energy to meet their net zero strategy goals.

Successful implementation requires experts who possess knowledge about climate science and skills for business transformation. A Chief Sustainability Officer who understands Paris Agreement pathways but cannot construct a finance-approved investment case produces reports rather than results.

A procurement director who negotiates contracts but lacks understanding of carbon markets cannot structure supplier agreements that allocate decarbonization risk appropriately.

Transition planning provides the blueprint for achieving net zero across the value chain. The International Energy Agency Net Zero Roadmap outlines sector-specific pathways toward 1.5°C alignment (4). The Science-Based Targets initiative provides validation mechanisms for corporate targets (5). However, organizations must develop internal capability to translate these frameworks into executable plans.

Finance teams cannot frequently model stranded asset risk under 2°C scenarios. Strategy teams may not quantify the competitive impact of carbon border adjustment mechanisms. Operations teams often lack analytical frameworks to determine which process modifications deliver the greatest emissions reduction per dollar invested.

A manufacturing company with a verified SBTi target must evaluate how capital allocation decisions affect its decarbonization pathway. The head of strategy leads a cross-functional intervention.

Important Tools to consider: Transition planning framework aligned with ISSB transition plan disclosure requirements (6), integrated into the existing capital budgeting system

Teams to integrate: Strategy, finance, operations, sustainability, investor relations

Result: Decision matrix embedding carbon reduction per investment dollar as a weighted criterion in capital expenditure approvals above a defined threshold; revised investment committee charter requiring climate scenario testing; updated financial planning model aligning capital deployment with pathway milestones

Absence of proper strategy causes:Incorrect deployment of capital enables companies to expand their operations which result in higher greenhouse gas emissions. The investors assess your environmental performance through carbon-adjusted returns which your competitors achieve at a higher level. Companies face regulatory noncompliance because their disclosure requirements have become more stringent. (6)

The manufacturer segments capital projects into three categories: essential decarbonization investments such as renewable energy and process electrification; business-as-usual investments with carbon implications, such as capacity expansion; and strategic bets involving new product lines or market entry. Applying carbon accounting criteria to each category makes emissions impacts visible within previously carbon-blind decision systems.

The organization reports an 18 percent increase in capital allocation toward decarbonization projects during the first planning cycle. Operational teams develop carbon fluency as emissions metrics become mandatory within budget submissions.

Net zero execution requires executive fluency in carbon markets. Carbon markets function both as compliance mechanisms and strategic instruments. Voluntary carbon markets allow companies to purchase verified emission reductions while their internal reduction capacity scales. The EU Emissions Trading System operates as a compliance market imposing emissions caps and financial penalties.

Leaders must distinguish between avoidance and removal credits, assess project integrity under the Integrity Council for the Voluntary Carbon Market Core Carbon Principles (8), and structure credit procurement strategies that complement, rather than substitute, direct reductions.

For example, an industrial firm preparing for SBTi validation structures its strategy across three horizons. Between 2025 and 2030, operational reductions are achieved through efficiency improvements and renewable sourcing. Between 2030 and 2040, supplier engagement and low-carbon materials drive value chain transformation. Between 2040 and 2050, residual emissions are addressed through certified carbon removal credits.

Finance integrates a rising internal shadow carbon price into investment appraisals. Procurement embeds carbon intensity standards within supplier scorecards. TCFD-aligned scenario analysis tests resilience under transition risk scenarios (7). The strategy relies on operational transformation rather than accounting adjustments.

Analysis published by Sustainability Magazine in April 2025, referencing LinkedIn’s 2024 Green Skills Report, indicates that the global economy will require approximately twice as many professionals with green skills by 2050 compared to current availability (2).

Organizations face a strategic decision: build internal capability or depend entirely on external consultants.

Consultants can deliver carbon inventories and transition roadmaps. However, once engagements conclude, organizations often lack internal expertise to update models, evaluate emerging technologies, or communicate transition plan adjustments to investors.

Internal capability development requires training finance teams in methodologies aligned with the GHG Protocol Corporate Accounting and Reporting Standard (9). Procurement professionals must learn supplier emissions evaluation and performance improvement program design. Operations managers must understand relevant ISO standards for energy management systems and their implementation.

Net-zero commitments require execution capability. Chartered Management Institute research shows that more than half of managers with net zero targets lack clarity regarding implementation responsibilities (1). Organizations understand goals but struggle to translate them into operational decisions.

The gap is not limited to climate literacy. Leaders must build financial models that withstand CFO scrutiny, design transition plans that endure regulatory examination, and structure credible carbon market strategies. Many sustainability programs emphasize frameworks without integrating financial modeling, capital allocation reform, and cross-functional influence.

The executive-level net zero courses in India equip professionals to convert commitments into measurable decarbonization outcomes. Effective sustainable development transformation programs strengthen leadership capabilities beyond ESG reporting obligations.

.webp)

.jpg)