Explore

ESG ratings, once seen as the backbone of sustainable investing, are now under intense scrutiny. As more capital flows into funds guided by environmental, social, and governance (ESG) scores, skepticism is growing about how those scores are assigned, what they measure, and whether they truly reflect a company’s sustainability performance.

In 2025, with trillions of dollars riding on these assessments, the lack of standardization, transparency, and accountability in ESG ratings has become one of the most debated issues in global finance. According to Bloomberg Intelligence, global ESG assets under management are projected to exceed $40 trillion by 2030, illustrating how rapidly sustainability-focused investments are expanding despite inconsistencies in scoring. Similarly, the OECD’s 2025 report on ESG ratings highlights a growing gap between corporate sustainability claims and the quality of underlying ESG data.

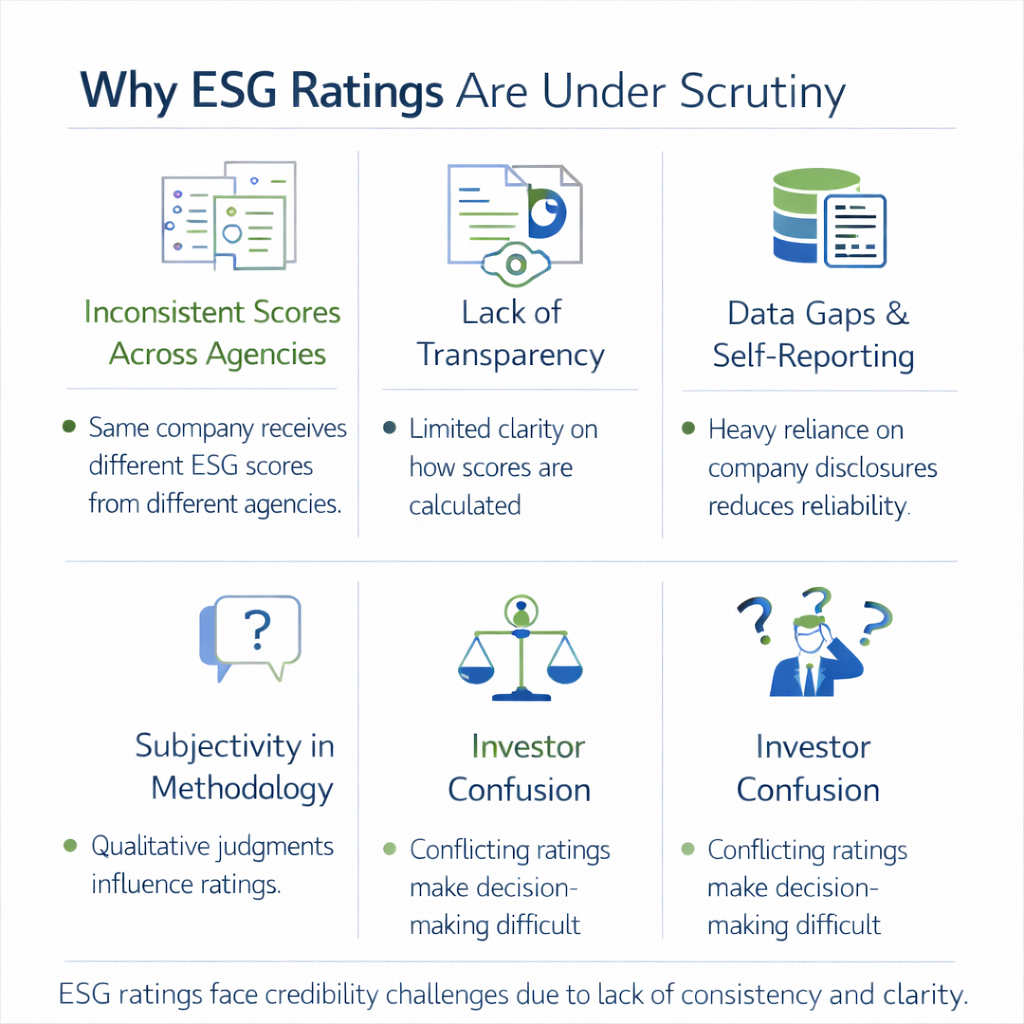

At the heart of the controversy lies a paradox: while ESG investing has grown exponentially, the ratings that underpin it remain fragmented and opaque. Different agencies can assign widely different ESG scores to the same company, leading to confusion among investors, misalignment of market signals, and growing distrust about the credibility of ESG claims. In India and other emerging economies, where ESG disclosure norms are still maturing, the stakes are even higher.

With regulatory bodies stepping in from the European Union’s proposal for regulating ESG rating providers (2024) to SEBI’s 2025 Master Circular on ESG Rating Providers (ERPs), this blog explores why ESG ratings are under the scanner, what reforms are underway, and how standardization could reshape the landscape of sustainable finance.

The global ESG rating ecosystem is diverse and decentralized. Dozens of agencies, ranging from global giants like MSCI, Sustainalytics, and S&P Global to niche analytics firms, use their own proprietary methodologies, weighting systems, and disclosure expectations. As a result, a company might receive an “A” rating from one agency and a “C” from another, with both assessments based on credible but non-aligned frameworks.

This divergence stems from several factors:

For investors, this lack of consistency undermines the very purpose of ESG ratings, that is, to serve as a reliable, comparative benchmark for risk-adjusted, sustainability-aligned investment decisions. For companies, especially those in developing markets, it creates reporting fatigue and uncertainty about what to disclose, to whom, and why.

Recognizing the risks of ESG rating inconsistency, regulators worldwide are beginning to intervene. The EU Taxonomy Regulation sets out a classification of sustainable economic activities for the EU market, aiming to anchor sustainable finance.

In India, SEBI has moved decisively. In January 2022, it released a consultation paper on ESG rating providers, followed by a Master Circular on ESG Rating Providers (ERPs) issued in July 2025.

Key regulatory moves include:

These developments mark an important shift. ESG ratings are no longer just market opinions; they are becoming part of the regulatory infrastructure of sustainable finance.

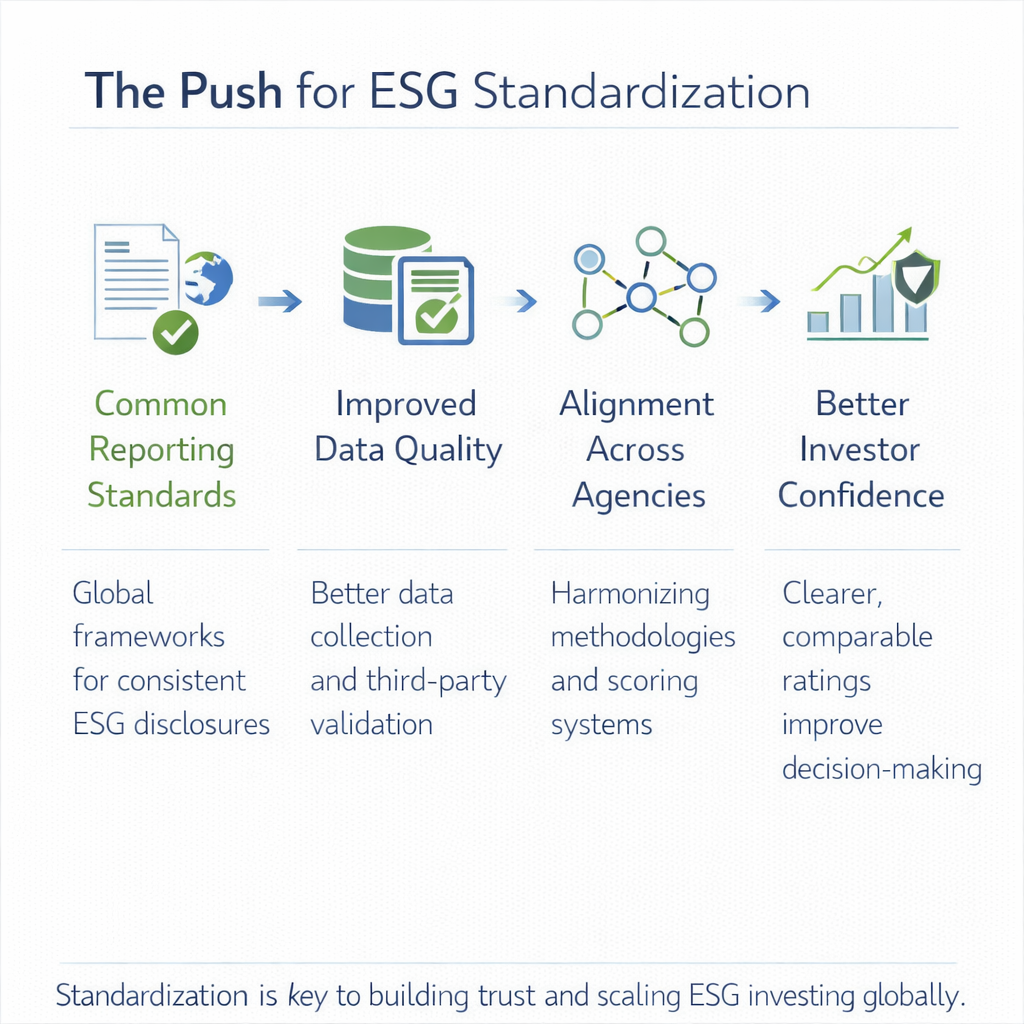

One way to achieve consistency in ESG ratings is through the adoption of common reporting and classification standards. The EU Taxonomy provides a way to anchor ratings in agreed-upon definitions of “green” or “transition” activities.

At the global level, the International Sustainability Standards Board (ISSB) is driving convergence in ESG disclosure, especially in climate-related financial risks. Similarly, India’s adoption of BRSR Core and TCFD-aligned reporting enhances rating comparability by ensuring consistent disclosure of emissions, governance, and climate strategies.

For ESG rating providers, aligning methodologies with these frameworks enhances credibility and fosters investor confidence across jurisdictions.

While standardization improves transparency, it is not without risks. There is a concern that ESG ratings might become overly mechanistic, focusing only on easily quantifiable metrics while ignoring qualitative impact or innovation. A mining company investing in indigenous rights, or an agri-tech firm with rural impact, may be overlooked if the rating system is too narrowly defined.

Moreover, standardization may favor large corporations with the resources to meet reporting requirements, while SMEs and startups could be excluded from sustainable finance flows due to limited compliance capacity.

To avoid this, ESG standardization must remain principles-based yet flexible, allowing for sectoral differences, regional priorities, and innovation in impact measurement.

India stands at an inflection point. By aligning ESG ratings with its taxonomy, climate roadmap, and stakeholder realities, it can set a global precedent for inclusive, credible, and context-aware ESG assessments. SEBI’s evolving regulations highlight that sustainability and ESG reporting are now central to corporate strategy and investment decisions.

In the climate economy, capital will chase credibility. In ESG, standardization may well be the strongest signal investors are waiting for.

As global investors and regulators demand greater accountability in sustainability disclosures, organizations need professionals who can navigate the complex landscape of ESG ratings, Net Zero strategy, and sustainable finance. Recognizing this shift, IIM Kashipur, in collaboration with evACAD, has launched the Post Graduate Executive Programme in Net Zero Strategy and Sustainability Leadership.

This program equips mid- and senior-level professionals with the strategic, analytical, and policy understanding needed to interpret ESG frameworks, lead sustainability reporting, and align business actions with global climate goals. Through modules on climate systems, green finance, carbon markets, ESG strategy, and circular economy, participants gain hands-on insights into how sustainable transformation is measured, managed, and communicated, bridging the very gaps discussed in this blog.

The journey of ESG ratings from fragmented, opaque scores to standardized, credible benchmarks is accelerating. For businesses, investors, and regulators, the question is no longer whether ESG matters, but how to measure, compare, and govern it.

Standardization is not just a compliance requirement; it is a strategic imperative for credibility and sustainable growth. For professionals aiming to lead in this evolving landscape, programs like IIM Kashipur’s executive course offer the perfect foundation to understand, strategize, and act in the new era of responsible business.

.webp)

.jpg)